Fitting probabilistic neural networks for regression

In the first article of this series, we discussed the use of NLL (Negative Log-Likelihood) as a loss function in the context of linear regression. We particularly showed that, under the assumptions of linear regression, NLL can be used to find the mean of the normal distribution that generates that data, achieving the same model as with MSE (Mean Squared Error).

When the data is linear and has a constant variance (homoscedasticity) that is independent of the independent variable $x$, linear models are generally suitable. However, when either or both of these conditions—linearity and constant variance—are not met, a linear model may underfit the data. In such cases, it’s often more convenient to relax these strict assumptions and consider more sophisticated models that can more accurately capture the distribution of the data. This will be the focus of this second article.

Relaxing the assumption about the constant variance of the residuals

In many datasets, the variance of the residuals is not constant but changes as a function of the independent variable. This phenomenon is known as heteroscedasticity.

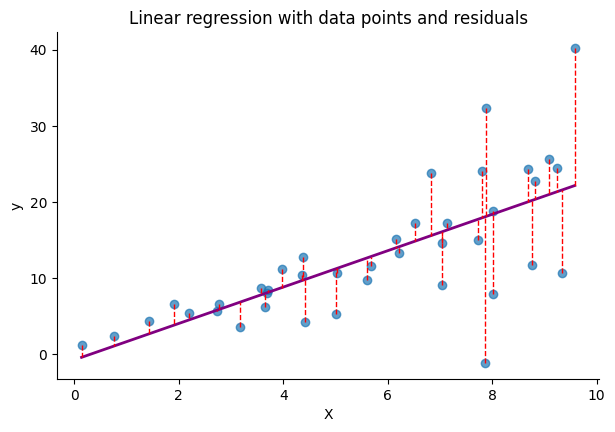

The following figure depicts data where the variance of the residuals increases as a function of $x$. As we can see, with the increase in $x$, the target values $y$ are more dispersed from the regression line. This implies that the range of potential values for $y$ widens, making the predicted value $\hat{y}$, which represents the model’s best estimate, less reliable.

In the case of a non-probabilistic model that is fitted using MSE, we lack a mechanism to assess the uncertainty of its predictions, implicitly treating all predictions as equally probable for any given value of the input $x$. On the other hand, with a probabilistic model, we can select a distribution that we believe accurately represents the data. The model is then tasked with predicting the parameters of this distribution for each input. By using the NLL as the loss function, we can effectively optimize the model to account for the uncertainty in its predictions.

In the previous article, we employed NLL to fit the mean of the Gaussian distribution representing the data. However, we did not estimate the other key parameter of the distribution, the standard deviation (std), under the assumption that the std of the residuals is constant across the data. We demonstrated that under this assumption, fitting a model using NLL is effectively equivalent to using MSE, as both methods aim to minimize the discrepancies between observed and predicted values.

In this second article, we’ll use NLL to fit both parameters of the Gaussian distribution (mean and std) to obtain a truly probabilistic model. This approach will allows us to evaluate the uncertainty of the model’s outputs. The steps to fit a probabilistic model include:

- Selecting a distribution family, which we assume represents the target variable $y$.

- Building a model, typically a neural network, that outputs the parameters $\theta$ of the chosen distribution for each input $x$. This model predicts the distribution parameters $\theta$ instead of directly predicting the target value $y$.

- Using a loss function, typically NLL, to tune the model’s parameters. This optimizes the model to maximize the likelihood of observing the target variable $y$ given the input $x$ and the distribution’s parameters $\theta$."

At this point, you may wonder: if the model predicts the parameters of a distribution, how do we obtain the final value $\hat{y}$? This value is typically the mean of the distribution, which is what the model was trained to predict in the previous article. Unlike a non-probabilistic model, we now have a method to compute the likelihood of this mean (as well as any other possible values) and assess the uncertainty associated with the model’s predictions.

Creating a model that predicts all the parameters of a Gaussian distribution

In the following, we create a simple linear model to predict the two parameters of the Gaussian distribution: the mean and the std. More precisely, the model outputs the mean and the logarithm of the std. We then apply the exponential function to the latter to ensure that it’s always positive. This model will allow us to fit data with a non-constant standard deviation, achieving a better NLL on validation data than a simple linear regression model.

Note that in the following code, unlike the first article, we’re not defining a proba_normal function and an NLL function that calls it and returns the negative log of the result. Instead, our NLL function now directly implements the negative of the log of the Gaussian distribution function.

# pytorch

import torch

import torch.nn as nn

from torch.optim import Adam

def NLL(y, mu, sigma=1):

a = -torch.log(sigma * torch.sqrt(torch.tensor(2 * torch.pi, dtype=torch.float64)))

b = (y - mu) ** 2 / (2 * sigma**2)

return -(a - b).mean()

def train_model(X, y, model, optimizer, loss_fn, n_epochs=1, log_at=0):

for epoch in range(1, n_epochs + 1):

y_hat = model(X) # y_hat is mu

mu = y_hat[:, 0]

log_sigma = y_hat[:, 1]

sigma = torch.exp(log_sigma)

loss = loss_fn(y, mu, sigma)

optimizer.zero_grad()

loss.backward()

optimizer.step()

if log_at <= 0:

continue

if epoch % log_at == 0:

print(f"Epoch {epoch}, loss: {loss.item():.4f}")

def predict(X, model):

with torch.no_grad():

return model(X)# tensorflow

import tensorflow as tf

from tensorflow import keras

from tensorflow.keras import backend as K

from tensorflow.keras import layers as tfkl

def NLL(y, theta):

mu, log_sigma = tf.split(theta, 2, axis=1)

mu, log_sigma = theta[:, 0], theta[:, 1]

sigma = tf.exp(log_sigma)

y = tf.squeeze(y)

a = -tf.math.log(sigma * tf.sqrt(tf.cast(2 * np.pi, "float64")))

b = (y - mu) ** 2 / (2 * sigma**2)

return -tf.reduce_mean((a - b))Then we initialize and fit our model:

# pytorch

model = nn.Linear(in_features=1, out_features=2, dtype=torch.float64)

optimizer = Adam(model.parameters(), lr=0.01)

X_t = torch.tensor(X, dtype=torch.float64)

y_t = torch.tensor(y, dtype=torch.float64)# tensorflow

K.set_floatx("float64")

model = keras.Sequential([tfkl.Dense(2)])

optimizer = keras.optimizers.Adam(learning_rate=0.01)

model.compile(optimizer=optimizer, loss=NLL)train_model(X_t, y_t, model, optimizer, NLL, n_epochs=1500, log_at=150)# tensorflow

model.fit(X, y, epochs=1500)Epoch 150, loss: 3.6933

Epoch 300, loss: 3.2984

Epoch 450, loss: 2.9245

Epoch 600, loss: 2.8238

Epoch 750, loss: 2.8009

Epoch 900, loss: 2.7838

Epoch 1050, loss: 2.7717

Epoch 1200, loss: 2.7640

Epoch 1350, loss: 2.7595

Epoch 1500, loss: 2.7568

Analyzing our model

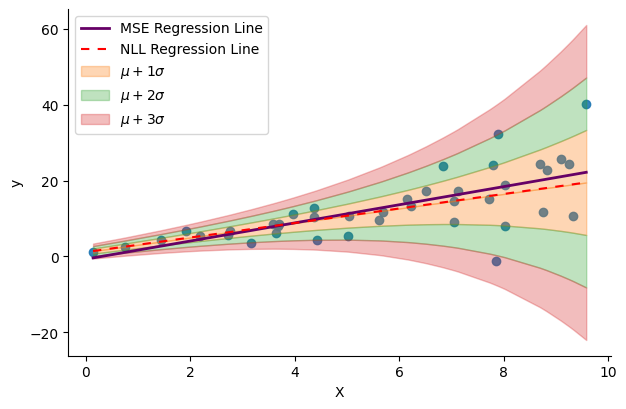

Let’s first apply prediction on the training data to compare our NLL-optimized model with the MSE-optimized model obtained using scikit-learn above. We will also focus on visualizing the std learned by the model, as it is our primary point of interest. The subsequent figure illustrates the regression lines of both models, alongside the data ranges covered by 1x, 2x, and 3x the magnitude of the learned std.

# pytorch

theta = predict(X_t, model).numpy()# tensorflow

theta = model.predict(X)mu = theta[:, 0]

sigma = np.exp(theta[:, 1])

plt.scatter(X, y, alpha=0.9)

plt.plot(X, y_hat, lw=2, c="#660066", label="MSE Regression Line")

plot_regression_line_with_std(X.squeeze(), mu, sigma)

plt.xlabel("X")

plt.ylabel("y")

plt.legend(loc="upper left")

The regression lines of the two models look slightly different. But importantly, the learned std seems to align well with the spread of the data and varies as a function of the input $x$. Now, the question is: does this make the NLL-optimized model any better than the MSE-optimized one? To answer this question, we generate some validation data and compute the validation loss for each model to make a more informed comparison

N = 4000

X_val = np.random.rand(N, 1) * 10

X_val = X_val[np.argsort(X_val.squeeze())]

var = np.linspace(0.0, 10, N)

y_val = 2 * X_val.reshape(-1) + 1 + np.random.randn(N) * varValidation loss of the NLL-optimized model

# pytorch

theta = predict(torch.tensor(X_val), model).numpy()# tensorflow

theta = model.predict(X_val)The following code creates a normal distribution (using scipy) for each data point based on the mean and standard deviation predicted by the model. It then computes the average NLL of all points. Furthermore, for purposes of comparison, we also calculate the validation MSE of the model.

from scipy.stats import norm

mu = theta[:, 0] # this is also y_hat, the model's best guess

sigma = np.exp(theta[:, 1])

dist = norm(mu, sigma)

nll_nn = -np.log(dist.pdf(y_val)).mean()

mse_nn = ((mu - y_val) ** 2).mean()

print(f"NLL: {nll_nn:.4}", f"MSE: {mse_nn:.4}")NLL: 2.971 MSE: 32.56

Validation loss of the MSE-optimized model

Given that this model doesn’t predict the std of the data, we can calculate the std of the residuals and use it to compute the NLL of the model on validation data.

mu = lin_model.predict(X_val)

sigma = np.std(mu - y_val)

dist = norm(mu, sigma)

nll = -np.log(dist.pdf(y_val)).mean()

mse = ((mu - y_val) ** 2).mean()

print(f"NLL: {nll:.4}", f"MSE: {mse:.4}")NLL: 3.176 MSE: 33.56

We can see that the NLL-optimized model outperforms the MSE-optimized for both loss metrics. Furthermore, this model enables us to compute the probability (density) of the predicted target values, allowing us to quantify the uncertainty associated with the predictions. We will delve deeper into this aspect in the final part of the article. In the next section, we’ll move beyond the assumption of data linearity and fit our first non-linear probabilistic regression model.

Relaxing the assumption about the linearity of the data

Dealing with non-linear data in regression problems is a very common in practice. One common way to tackle such problems using neural networks is using non-linear activation functions. Moreover, depending on the complexity of the data, increasing the network’s representation capacity by stacking more layers and increasing the number of parameters within the layers can be useful. In the following, we will generate some non-linear data and fit a neural network with two layers and a non-linear activation after the first layer.

# pytorch

model = nn.Sequential(

nn.Linear(1, 16, dtype=torch.float64),

nn.SELU(),

nn.Linear(16, 2, dtype=torch.float64),

)

optimizer = Adam(model.parameters(), lr=0.01)

X_t = torch.tensor(X, dtype=torch.float64)

y_t = torch.tensor(y, dtype=torch.float64)# tensorflow

model = keras.Sequential(

[tfkl.Dense(16, activation="selu"),

tfkl.Dense(2)],

)

K.set_floatx("float64")

optimizer = tf.keras.optimizers.Adam(learning_rate=0.01)

model.compile(optimizer=optimizer, loss=NLL)# pytorch

train_model(X_t, y_t, model, optimizer, NLL, n_epochs=1000, log_at=100)# tensorflow

model.fit(X, y, epochs=1000)Epoch 100, loss: 0.1186

Epoch 200, loss: -0.2046

Epoch 300, loss: -0.6314

Epoch 400, loss: -0.7417

Epoch 500, loss: -0.7756

Epoch 600, loss: -0.8026

Epoch 700, loss: -0.8178

Epoch 800, loss: -0.8276

Epoch 900, loss: -0.8360

Epoch 1000, loss: -0.8441

# pytorch

theta = predict(torch.tensor(X), model).numpy()# tensorflow

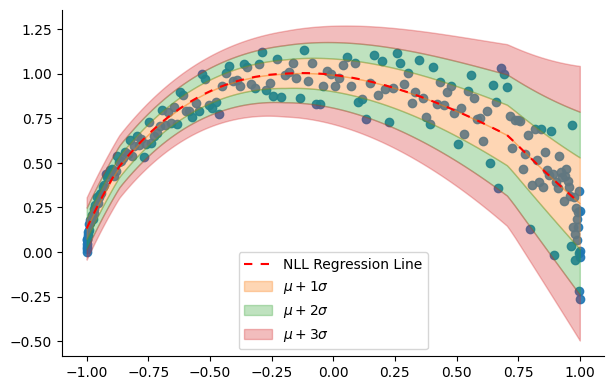

theta = model.predict(X)The figure below displays the regression line produced by the model along with the varying std that it has learned.

mu = theta[:, 0]

sigma = np.exp(theta[:, 1])

plt.scatter(X, y, alpha=0.9)

plot_regression_line_with_std(X.squeeze(), mu, sigma)

plt.legend(loc="lower center")

A Practical example: forecasting the next US president using economic growth

In this section, we use data collected by political scientist Douglas Hibbs, as introduced in the book Regression and Other Stories, chapter 7, by Gelman, Hill, and Vehtari. The dataset is available for download from the book’s official repository.

Hibbs developed a model known as “Bread and Peace” to forecast US election outcomes based on economic growth as the only feature (with adjustments made for wartime conditions). The data is presented in the table below, where vote represents the incumbent party’s vote percentage, and growth denotes the average personal income growth during the years leading up to the vote.

import pandas as pd

data = pd.read_csv("data/hibbs.dat", delimiter=" ")

data| year | growth | vote | inc_party_candidate | other_candidate |

|---|---|---|---|---|

| 1952 | 2.40 | 44.60 | Stevenson | Eisenhower |

| 1956 | 2.89 | 57.76 | Eisenhower | Stevenson |

| 1960 | 0.85 | 49.91 | Nixon | Kennedy |

| 1964 | 4.21 | 61.34 | Johnson | Goldwater |

| 1968 | 3.02 | 49.60 | Humphrey | Nixon |

| 1972 | 3.62 | 61.79 | Nixon | McGovern |

| 1976 | 1.08 | 48.95 | Ford | Carter |

| 1980 | -0.39 | 44.70 | Carter | Reagan |

| 1984 | 3.86 | 59.17 | Reagan | Mondale |

| 1988 | 2.27 | 53.94 | Bush, Sr. | Dukakis |

| 1992 | 0.38 | 46.55 | Bush, Sr. | Clinton |

| 1996 | 1.04 | 54.74 | Clinton | Dole |

| 2000 | 2.36 | 50.27 | Gore | Bush, Jr. |

| 2004 | 1.72 | 51.24 | Bush, Jr. | Kerry |

| 2008 | 0.10 | 46.32 | McCain | Obama |

| 2012 | 0.95 | 52.00 | Obama | Romney |

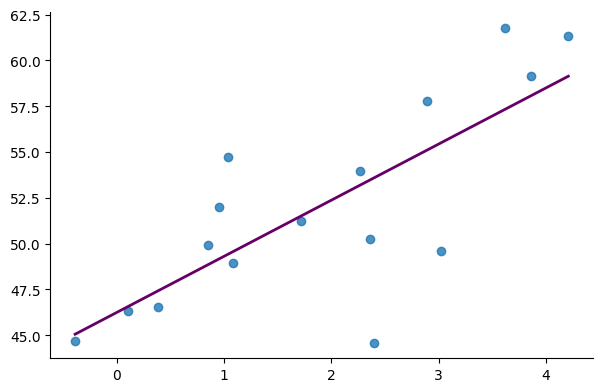

The figure below displays the dataset along with the linear model developed by Hibbs:

A probabilistic model for Hibbs’ data

In the following, we’ll build a probabilistic neural network to model Hibbs’ data. Leveraging the flexibility of neural networks, we will make a slightly different architectural choice for our model compared to the previous one. We will use a linear branch of the network to predict the mean of the distribution (representing the model’s best guess), and a non-linear branch to predict the std, allowing our model to adapt to the varying spread of data points across different values of $x$.

# pytorch

class ProbModel(nn.Module):

def __init__(self, n_units=64):

super().__init__()

self.hidden = nn.Linear(1, n_units)

self.mu_output = nn.Linear(n_units, 1)

self.log_sigma_activation = nn.SELU()

self.log_sigma_output = nn.Linear(64, 1)

def forward(self, X):

out = self.hidden(X)

mu = self.mu_output(out)

log_sigma = self.log_sigma_output(self.log_sigma_activation(out))

return torch.stack([mu, log_sigma], axis=1).squeeze()

def predict(self, X):

X = torch.tensor(X)

with torch.no_grad():

return self(X).numpy()# tensorflow

class ProbModel(keras.Model):

def __init__(self, n_units=64, **kwargs):

super().__init__(**kwargs)

self.hidden = tfkl.Dense(n_units)

self.mu_output = tfkl.Dense(1)

self.log_sigma_activation = keras.activations.get("selu")

self.log_sigma_output = tfkl.Dense(1)

def call(self, X):

out = self.hidden(X)

mu = self.mu_output(out)

log_sigma = self.log_sigma_output(self.log_sigma_activation(out))

return tf.squeeze((tf.stack([mu, log_sigma], axis=1)))# pytorch

model = ProbModel()

optimizer = Adam(model.parameters(), lr=0.01)

X_t = torch.tensor(X, dtype=torch.float32)

y_t = torch.tensor(y, dtype=torch.float32)# tensorflow

model = ProbModel()

K.set_floatx("float64")

optimizer = tf.keras.optimizers.Adam(learning_rate=0.01)

model.compile(optimizer=optimizer, loss=NLL)# pytorch

train_model(X_t, y_t, model, optimizer, NLL, n_epochs=4000, log_at=400)# tensorflow

model.fit(X, y, epochs=1000)Epoch 400, loss: 5.3124

Epoch 800, loss: 5.1888

Epoch 1200, loss: 4.6035

Epoch 1600, loss: 3.9734

Epoch 2000, loss: 3.4727

Epoch 2400, loss: 2.5117

Epoch 2800, loss: 2.4196

Epoch 3200, loss: 2.2628

Epoch 3600, loss: 2.1138

Epoch 4000, loss: 2.2820

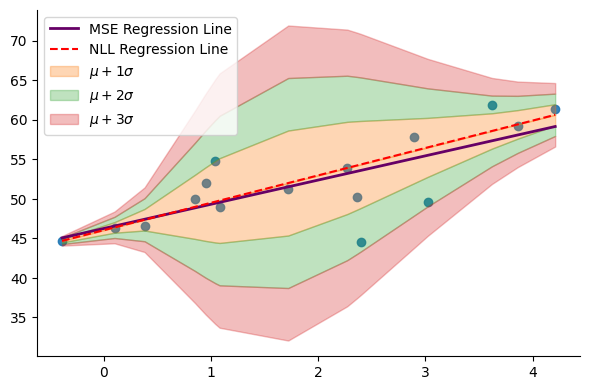

Analyzing our model

Let’s begin by plotting the obtained model:

theta = model.predict(X)

mu = theta[:, 0]

sigma = np.exp(theta[:, 1])

plt.scatter(X, y, alpha=0.9)

plt.plot(X, y_hat, lw=2, c="#660066", label="MSE Regression Line")

plot_regression_line_with_std(X.squeeze(), mu, sigma)

plt.legend(loc="upper left")

The model effectively captures the varying spread of the data, with the highest level of uncertainty occurring within the growth interval between 2 and 3. Consequently, it is advisable to approach predictions made by the model (represented by the red dashed line, indicating the mean of the distribution) with caution. This observation aligns with our intuition after analyzing the data, indicating that relying solely on growth as a feature may not be sufficient for predicting voting outcomes, and additional features may be necessary.

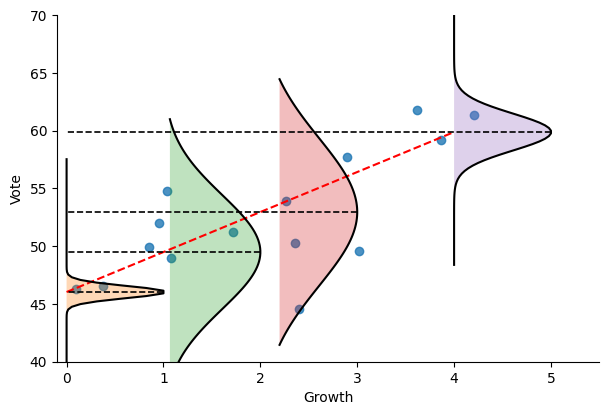

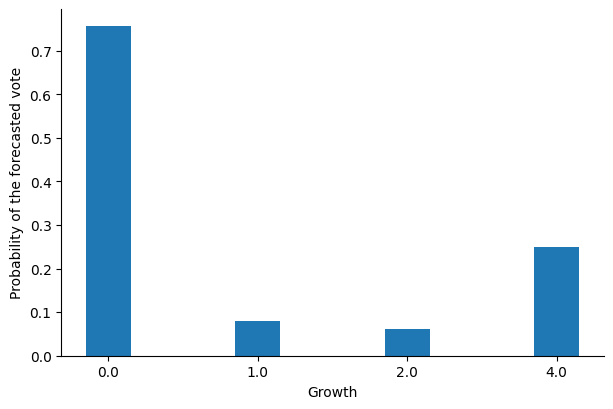

Let’s now visualize the obtained distributions at four different growth levels: 0, 1, 2, and 4. The distributions appear narrower at very low and very high growth levels:

We can use these distributions to calculate the probability density of the model’s best estimate (i.e., the mean of the distribution) at these specific points:

We can see that the model is much less certain about its predictions for growth values equal to 1 and 2, suggesting that we should be careful when using these predictions and that other (unknown) variables are required to determine the outcome of the voting outcome.

Getting the most out of the model

While obtaining the model’s best estimate and evaluating its uncertainty is valuable, there is room for improvement in this specific dataset and problem. Instead of solely predicting the incumbent party’s candidate’s vote share, we can calculate the probability of that candidate winning the election, defined as receiving more than 50% of the votes. This can be achieved by computing the Cumulative Distribution Function (CDF) for a vote share equal to 50 (i.e., the probability that a value is less than 50 in the given distribution) and subtracting it from 1:

$$p(vote > 50) = 1 - p(vote \le 50) = 1 - CDF(50)$$

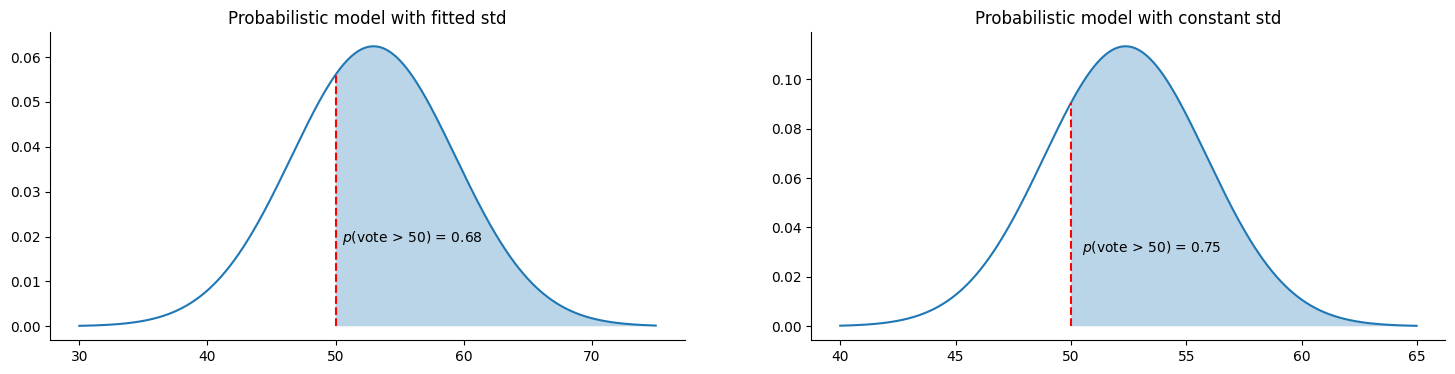

Now, let’s examine the 2016 vote, which was between Hillary Clinton (the candidate of the incumbent party) and Donald Trump. The economic growth in the period preceding the vote was approximately 2.0 (this data point was not part of the training dataset). According to the probabilistic model, Clinton is predicted to receive a vote share of 52.96%—this value may be different, depending on the model you obtained after training— while the non-probabilistic model predicts a vote share of 52.37%.

growth = np.array([[2]], dtype=np.float32)

print(f"Prob. model: {model.predict(growth)[0]:.2f}")

print(f"Non-prob. model: {lin_model.predict(growth)[0]:.2f}")Prob. model: 52.96

Non-prob. model: 52.37

We define a helper function to calculate and visualize the probability of winning, $p(vote > 50)$, based on each model’s predictions. For the non-probabilistic model, we use the std of the residuals from the training data.

fig = plt.figure(figsize=(18, 4))

theta = model.predict(growth)

mu = theta[0]

sigma = np.exp(theta[1])

dist = norm(mu, sigma)

plt.subplot(1, 2, 1)

plot_dist_and_proba(dist, 30, 75, 50)

plt.title("Probabilistic model with fitted std")

# compute the std of the residuals

residuals = lin_model.predict(X) - y

sigma = np.std(residuals)

# compute the mean (a.k.a. model prediction) at growth = 2

mu = lin_model.predict(growth)[0]

dist = norm(mu, sigma)

plt.subplot(1, 2, 2)

plot_dist_and_proba(dist, 40, 65, 50)

plt.title("Probabilistic model with constant std")

Both models predict a relatively high probability of Clinton winning. As this vote is now a part of history, we know that both models’ predictions were incorrect. The probabilistic model, fitted with NLL, yields a lower probability of winning, mainly due to the higher spread of data points around a growth value of 2. It’s important to note that the specific probability from the probabilistic model may vary depending on the model obtained after training.

Summary

Probabilistic regression models are created by fitting all the parameters of the distribution assumed for the data. Once fitted, these models can be used to predict the target value and evaluate the uncertainty associated with the prediction. The flexibility of neural networks allows us to choose how to fit each parameter of the distribution: linearly or non-linearly. Depending on the problem at hand and dataset, probabilistic models can be used to make more informative decisions, as demonstrated in the voting example above (e.g., using 1-CDF).